Making Cents: How to Develop Your Financial Preparedness Skill-Set

Making Cents: How to Develop Your Financial Preparedness Skill-Set

As most of you know, we believe in being prepared here at ITS. From knowing how to tie knots, build a fire and having good situational awareness, being prepared will dramatically enhance your experiences in life. Waiting until the last minute will constantly cost you something; whether it’s your time, money or in serious cases, even your life.

This is why it’s important to be the right person for the job before you hold the job title. It’s also why spending even small amounts of time educating yourself instead of “liking” your buddy’s kitten photo on Facebook will pay dividends when you find yourself facing the unexpected.

Today we’re going to venture off of the beaten path of what we usually publish at ITS and discuss something that’s less about staying alive and more about living well. Our personal finances limit us daily in ways like nothing else can. Our physical health, hobbies, cool gear and so much more is limited by one key factor, our money. So why is it that people who carry concealed, keep a medical kit on them at all times and can tie the most complicated of knots, still don’t invest in their retirement?

This doesn’t make any sense. If you’re banking on Social Security being intact by the time you need it, then you’re barking up the wrong tree. Forbes Magazine recently published that by the year 2033 the U.S. will be out of reserves to pay Social Security and that taxes may only be enough to pay for 75% of the promised benefits.

To compensate for this, the rest of the shortfall would be made up with a gradual increase in the “full” or “normal” retirement age for Social Security. This means less generous benefits for the highly paid and decreasing the annual cost of living increases for the already retired by about 0.3 percentage points a year. An upward adjustment wouldn’t come until a beneficiary had been on Social Security for 20 years, in order to soften the cumulative effects.

Social Security will be harder to get if it’s still around and it should absolutely NOT be depended upon. There are many reasons why you need to start addressing the retirement problem now. You can never be too early, but you can be too late. In the words of Dave Ramsey, “You need to live like no one else today, so that you are able to live like no one else tomorrow.” While it takes proper planning, teamwork and personal discipline, planning for retirement will give you a peace of mind by ensuring you won’t be a burden to your loved ones.

The Mission

You certainly can’t build Rome in a day and you definitely can’t build wealth that quickly either; it’s similar to personal fitness, actually. To elaborate on this analogy, let’s say you haven’t been working out regularly, but then crush the workout of your lifetime, you might get injured or at the very least disillusioned. However, if you build short, medium and long term goals that are catered to your specific situation and current standing, then you are much more likely to succeed.

In fitness, the most important thing to do is get started. If you build a routine into your lifestyle, after awhile healthy living becomes a habit and the positive effects are felt throughout your entire lifetime. This is true for your financial situation as well.

I admit that I’m not a financial guru and while I’ve been through business school, I learned enough about accounting to know how to hire a good accountant. That said, we’re blessed here at ITS to have some very impressive people with a wide variety of knowledge as part of our family. In fact, the idea for this article was a collaboration with Tim Anderson, a long time ITS member and regular attendee to our annual Muster where he earned the nickname, “The Jeweler,” which has stuck with him for years.

Tim is a licensed CPA, a Chartered Global Management Accountant (CGMA) and holds the Accredited Investment Fiduciary designation. He’s been gaining experience throughout his lifetime and has worked as much overseas as he has domestically. Currently he’s the Managing Director at Halbert Hargrove Global Advisors, LLC, a Fiduciary Investment Management and Wealth Advisory firm.

The Method

Tim suggests a great place to start getting financially fit is thinking about what financial goals you might have, formulating them and then writing them down and keeping them for periodic review and revision. As your financial goals evolve, so will your written ones. It’s also helpful to break them up into short, intermediate and long-term goals. That way, the eventual strategies you map out to reach your goals become more specific and reaching them is more probable.

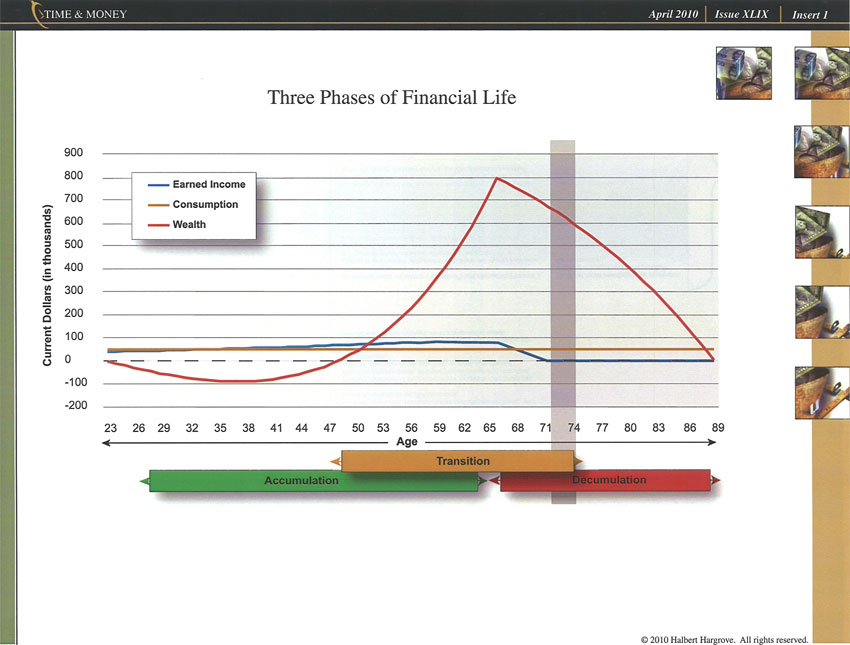

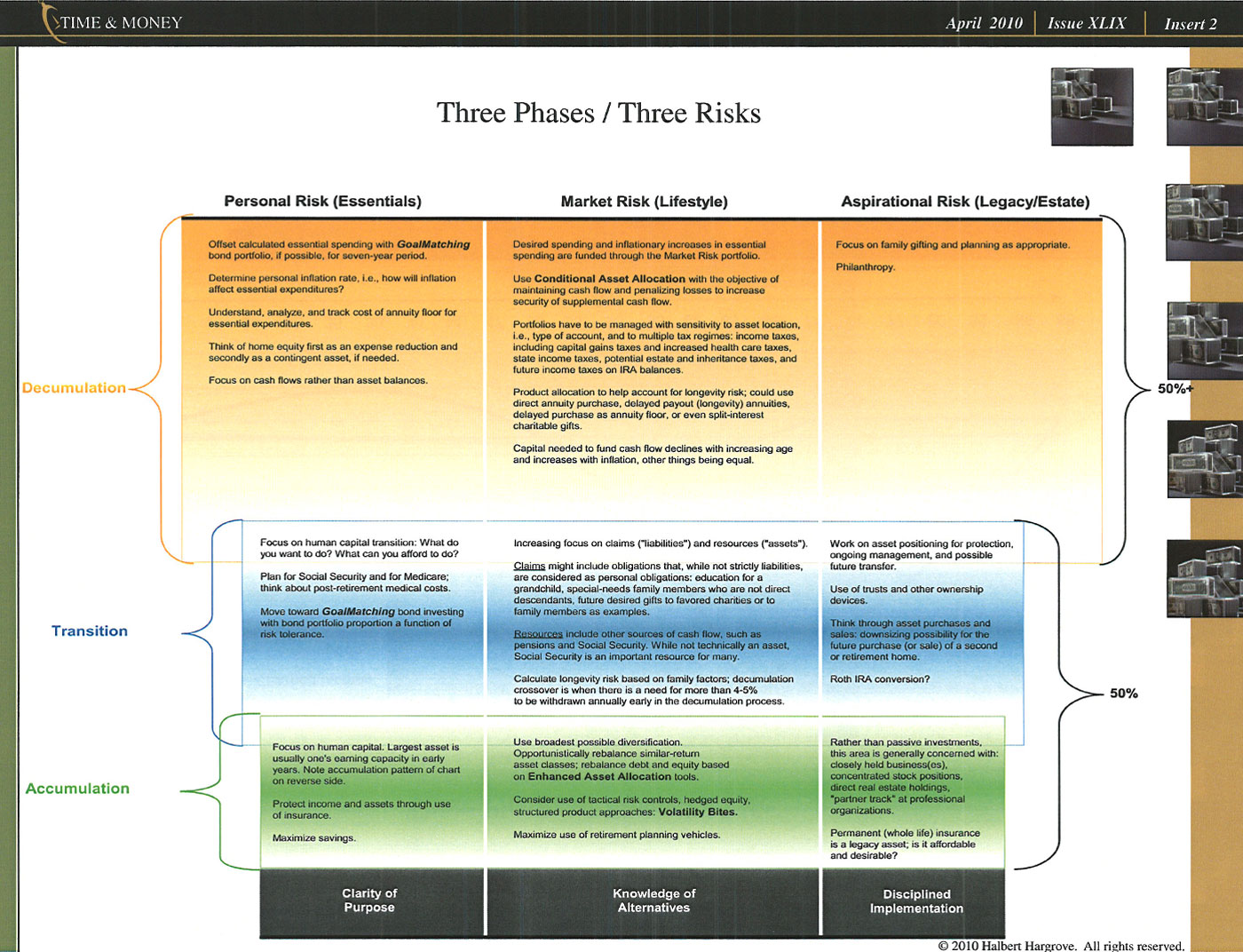

Like many forms of preparedness, it can be a life-long pursuit, so it’s helpful to take stock of where you are. Most of us start out earning income in our teens to twenties and the average American then goes on to work an entire career. Throughout that career, you may want to consider whether you’re in an accumulation mode, transition mode or a decumulation mode.

Accumulation usually ranges from the beginning of work life to roughly the mid 60’s. Transition usually runs from the late 40’s to the mid 70’s and Decumulation from the late 60’s to the end of life. Accumulation through Transition is the saving period in life and Decumulation is the spending period.

It’s a guess that most of you reading this are likely to be “accumulators,” but there are a lot of things you can do at any income level to start accumulating. Using the concept of “pay yourself first,” make your savings account the first “bill” you pay each billing period. Even if it’s $5 a week, the point is to save something. The most tax-efficient way to save is with an employer who sponsors a (tax) qualified savings plan.

Using a company sponsored savings plan not only reduces current income taxes, but forces you to save something for the future. Currently, individuals with such plans can save up to a maximum of $15,500 per year. If there’s a company matching contribution, you’re only leaving money on the table by not participating. For example, if you contribute 3% of your income and the company matches 3%, you have a 100% rate of return on your money before even investing it.

If you don’t contribute at least equal to the match, you’re leaving money on the table. If you don’t have a company sponsored plan, use an IRA; you can put away up to $5500 per year pre-tax. (Those over age 50 can add an additional $1000 to those contribution limits.) These are good tools whether you’re an employee of a company or an entrepreneur.

Managing Risk

The tax incentive provided by Congress is there, on purpose, to incentivize us to save. Understandably, we all come from different fields, levels of income and means. However, here it only matters IF you “train,” rather than how hard. Saving anything at all gets you in the financial preparedness game. If you work at this over an entire career, throw in the miracle of compounding interest over the course of several decades and you’ll be going a very long way toward being able to deal with the biggest risk we all face: outliving our money.

This is called “Longevity Risk” and as our average life spans increase and the future prospects for Social Security continue to look bleak, this is a very real risk. The problem with this risk is that it rears its head in the future and because of that, it’s often ignored.

There are also other risks that one should take stock of and consider threats to your accumulation plans. These financial surprises cost us money. However, many of these risks can be transferred to another party. For example, if you’re a homeowner, you can insure your home against loss. You’re also now required to insure your health (or risk penalty) and hopefully you insure your firearms!

You can also purchase liability insurance for your car. Without the ability to pay the insurer to take that risk from you, you’d have to finance the risk yourself. The idea here is that financial risk management is important too, so that your accumulation plans don’t get derailed by inevitable financial surprises in life. If you have insurable risks and you can afford it, buy the insurance.

As life marches on, life events such as marriages, children, divorce and death occur. With these events, comes the need to go back to the written goals to review and revise, according to the curve you’ve been forced to negotiate. What they then become is your operating framework to help you change course and develop new paths to achieve your goals, or even formulate new ones. Even if your life is smooth sailing for a while, periodically returning to review your goals serves to help you monitor your progress toward them.

Implementation

Having a goal setting framework, saving discipline and financial risk management in place is your embarkation point. From there, you need to decide what to invest in. This should be exclusively a personal decision about how much risk you’re willing to take. (Or, thinking about how much of it you might be willing to lose.) There are many so-called “rules of thumb” out there, based upon age and income levels, but those recommendations are usually geared to a wide audience.

While these general recommendations offer some frame of reference, it’s far better to get specific about yourself. Some people get a kick out of investing, but usually only when the financial markets are advancing; sell-offs like the credit crisis in 2008 are great equalizers. Tim’s philosophy is to stay as diversified as possible at the lowest expense possible.

There are many ways to go about this. Most company sponsored savings plans use mutual funds; you pay for active management, but the presumption is that your employer has followed standards of fiduciary care in selecting and monitoring such funds. Indeed, they are legally held to these standards under federal pension legislation, so you can place some confidence in their selections.

Outside of these employer sponsored plans, though, you’re on your own in terms of conducting due diligence over investments. However, by simply staying broadly diversified in your asset mix, you’ll be doing a lot to add shock absorption to your portfolio and you’ll be managing a larger number of eventual market outcomes than you otherwise would be with a more concentrated mix of assets. Tim also favors broad asset class exposure as opposed to picking individual stocks (although it’s not nearly as much fun).

When it comes to future livelihood, Tim feels boring and non-heroic is a better way to go. When it comes to bragging rights about your investments, go ahead and pick stocks, but in the end the tortoise will win because the financial investment markets have proven, over time, that they are very good at transferring wealth from impatient undisciplined investors to the patient disciplined ones.

Some employer plans also use indexed positions (called “passive” investing), or a combination of passive and professionally managed (called “active” investing) positions, which can lower the cost of investing and are broadly diversified and very liquid.

If you don’t have an employer plan, you can still do this on your own, it will just take a bit of your time, some careful planning and some ongoing discipline to make it work. Another alternative is to hire an advisor if you don’t have the time or inclination to do it yourself. If you go that route, make sure you ask for references and actually call them. Also, go on to the SEC website EDGAR section and check for complaints and read their “ADV.”

Anyone registered to invest for the public has an “ADV,” which is a disclosure document about the advisor and their firm. It shows ownership, billing policy, investment philosophy and strategy. If you don’t find one for them, don’t use them; you will have saved yourself a lot of expensive grief.

Hiring an advisor is a tough decision, because one always wonders if they’re getting good value for the money they’re paying the advisor. That’s an individual value judgement and should be weighed against an honest self-evaluation of whether you can truly invest on your own, or should get an advisor to help you maintain the discipline.

A good advisor will act as your guide, guru or gladiator depending upon your needs and they’ll work hard to see that you’re understood and supported. If they’re disciplined about their work, they’ll probably do right by you.

Tim admits a bias here. Advisors who work for large publicly traded companies have a built-in flaw in their business model; their first legal fiduciary duty is to their employer, not to their client. An advisor that’s privately owned is free to operate as they wish and while they may not necessarily be completely free of conflicts of interest, at least they’ll have their own reputation and business longevity at stake. It’s just a better alignment of incentives that can work in your favor instead of against you.

Other Considerations

Following a “disciplined financial training process” if done consistently will yield results. You’ll accumulate assets and be surprised at how far you’ll get in just a few years. Over a lifetime, many people accumulate a large amount of assets and will need to ensure that any left over after they go to that “Great Muster In The Sky” will end up where they want them to end up. Writing down your wishes and in some cases, getting a lawyer specializing in estate planning to help you choose the right words for this purpose, is worth the money spent to have it done right.

Also, choosing the right person to carry out these instructions is important, as you’ll need to trust that they’ll do as you wish. They’ll also have a legal obligation to carry out your wishes, or risk being in violation of fiduciary duty and get in legal hot water. Be sure that who you select is willing to do it right.

The next step is getting this document notarized and recorded with the county recorder so it becomes legally binding and the person you entrust to carry out your wishes is given the legal power to manage your assets until distributed according to your written wishes. Laws change too though, so remember to review this document every 5 years or so.

Another important consideration is whether you’ve accumulated enough assets that you want to leave some of them to an educational, social, religious or other worthy institution. Or, if you’ve built a business and wish to pass it along to children or others close to you, it must be expressed in writing so that the executor of the estate can ensure it’s done legally and properly.

Legacy issues like these can seem a long way off, but time goes by quickly and sometimes we find ourselves wondering how we got here. Thinking about about this possibility now will be good planning and discipline. If you’re one of these people, you may want to consider the idea that because you’ve been fortunate enough to accumulate so much, you have a responsibility to handle your resources prudently like this.

On the down side, life can also be a bit of a soup sandwich sometimes and stressed finances only make things harder. All kinds of things can cause this, but the big ones are having dependent adult family members and special needs dependents. If your life includes these issues, they’ll need to be imported to your planning and play a central role in establishing your goals.

Lastly, similar to how you might diversify your investments to mitigate the loss of concentrated bets, you might also consider diversified income streams to add security to total combined income. For example, Social Security was mentioned earlier. While no one knows the eventual outcome of this political hot potato and if for some reason it’s still around when we’re ready for it, it will represent another source of income over and above what we draw from our savings.

Another few examples might be what you receive in the way of a pension for long service to an employer, or what you might earn from private business or real estate investments accumulated along the way.

Conclusion

Preparing ourselves for the future now will alleviate the pressures that will certainly come when we lose the ability to work as we grow older. Additionally, if we choose to be wise in our savings, our children will benefit from seeing our example.

Knowledge is power and in this case, the power will lead to a more fulfilling and happy life. I encourage our readership to take Tim’s advice and run with it. Putting a fraction of your earnings away and listening to sound advice will go a long way and is worth the time. Let’s get going!

Discussion